Table Of Content

- Capital gains tax on real estate and selling your home

- Capital Gains Tax Exclusion for Homeowners: What to Know

- Colombo Stock Exchange: Most Sustainable Growth Exchange Asia

- Capital gains, losses, and sale of home

- Qualifying for the exclusion

- Poles Apart: TGE has Created its Own Space in the Energy Market

You can also add sales expenses like real estate agent fees to your basis. Subtract that from the sale price and you get the capital gains. When you sell your primary residence, $250,000 of capital gains (or $500,000 for a couple) are exempted from capital gains taxation. This is generally true only if you have owned and used your home as your main residence for at least two out of the five years prior to the sale.

Exchange Rates and Capital Gains on Your Mexican Home - Mexperience

Exchange Rates and Capital Gains on Your Mexican Home.

Posted: Wed, 27 Mar 2024 07:00:00 GMT [source]

Capital gains tax on real estate and selling your home

An earlier version of this story gave an example of capital gains taxation that stated $200,000 would be the amount paid in capital gains tax on a $500,000 asset sale. The story has been updated to state $200,000 is the taxable portion of the capital gain, not the total amount paid. Conclusion President Biden’s proposal to raise capital gains rates has ignited debate and speculation. While the headline rate of 44.6% is eye-catching, the full impact of the proposal depends on a range of factors, including income thresholds, exemptions, and legislative outcomes.

Capital Gains Tax Exclusion for Homeowners: What to Know

For single filers, earnings up to $47,025 are taxed at 0%, with incomes between $47,025 and $518,900 taxed at 15% and above $518,900 at 20%. You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

Colombo Stock Exchange: Most Sustainable Growth Exchange Asia

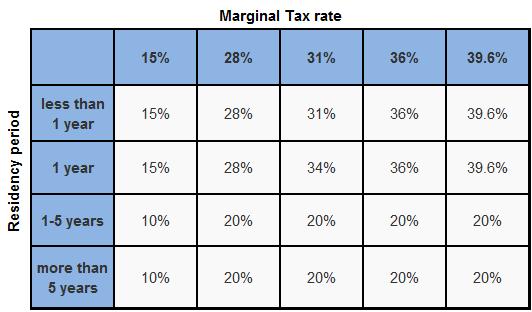

You could, for example, purchase the house, live in it for 12 months, rent it out for a few years and then move in to establish primary residency for another 12 months. As long as you lived in the property as your primary residence for 24 months within the five years before the home’s sale, you can qualify for the capital gains tax exemption. And if you’re married and filing jointly, only one spouse needs to meet this requirement.

Capital gains, losses, and sale of home

One strategy to maximize your tax benefits is converting your second home into your primary residence for at least two of the five years preceding the sale. This move can qualify you for a partial exclusion of the capital gains tax, leveraging the aforementioned $250,000 or $500,000 exclusions, depending on your filing status. If you own a home, you may be wondering how the government taxes profits from home sales.

But if you invest part of the gains, only that portion of the gains contributed to the QOF qualifies for deferral. This tax break doesn't apply to main homes or vacation homes, but it can apply to rental real estate that you own. Recourse debt is when the debtor remains personally liable for any shortfall. If the lender forgives the remaining debt, a special tax rule provides that up to $750,000 in forgiven debt on a primary home is tax-free. The debtor will be taxed on any remaining forgiven debt at ordinary income tax rates up to 37%. Net capital gains are taxed at different rates depending on overall taxable income, although some or all net capital gain may be taxed at 0%.

Ask Nancy: Should I sell my cottage and investment property now instead of next year? - The Globe and Mail

Ask Nancy: Should I sell my cottage and investment property now instead of next year?.

Posted: Fri, 26 Apr 2024 16:52:43 GMT [source]

Some say it should be taxed at a rate higher than the earned income tax rate, because it is money that people make without working, not from the sweat of their brow. Others think the rate should be even lower than it is, so as to encourage the investment that helps drive the economy. You also don’t need to worry about capital gains if you’re buying a house, at least not yet. If you plan to sell your new home sometime down the road, though, you’ll have to consider the tax implications of that transaction. Don’t hesitate to ask a tax advisor for help if you’re confused at all about your tax liability.

Poles Apart: TGE has Created its Own Space in the Energy Market

Generally, capital gains and losses occur when you sell something for more or less than you spent to purchase it. Gain from the sale or exchange of your main home isn’t excludable from income if it is allocable to periods of nonqualified use. Nonqualified use means any period after 2008 where neither you nor your spouse (or your former spouse) used the property as your main home, with certain exceptions.

What if my home sells at a loss?

If you don’t have a bank account, go to IRS.gov/DirectDeposit for more information on where to find a bank or credit union that can open an account online. See Form 5405, Repayment of the First-Time Homebuyer Credit, to find out how much to pay back, or if you qualify for any exceptions. If you do have to repay the credit, file Form 5405 with your tax return. If you granted someone an option to buy your home and it expired in the year of sale, report the amount you received for the option as ordinary income. Use the following method to compute your real estate tax deduction, which may be different from the amount of real estate tax you actually paid.

It is also important to consider any state or local taxes that may apply to the sale of your home. Angela Rayner is expected to claim that she was not required to pay capital gains when she sold her former council house after offsetting the tax with a kitchen renovation. Tax experts have told The Telegraph that if Mr Rayner was liable to pay capital gains tax, the bill would depend on factors such as income, renovations and estate agent fees, but would likely only be about £500.

The list is not exhaustive, as the rules for this exclusion can be complex. If you have questions, consider reviewing Publication 523 or speaking with a tax advisor. Fortunately, the Taxpayer Relief Act of 1997 provides some relief to homeowners who meet certain IRS criteria. For single tax filers, up to $250,000 of the capital gains can be excluded, and for married tax filers filing jointly, up to $500,000 of the capital gains can be excluded.

As with other assets such as stocks, capital gains on a home are equal to the difference between the sale price and the seller's basis. Why the difference between the regular income tax and the tax on long-term capital gains at the federal level? It comes down to the difference between earned and unearned income. In the eyes of the IRS, these two forms of income are different and deserve different tax treatment.

However, see Table 1 below to determine if any exceptions to this rule listed in the “IF” column apply. To figure the gain or loss on the sale of your main home, you must know the selling price, the amount realized, and the adjusted basis. Subtract the adjusted basis from the amount realized to get your gain or loss. Generally, if you transferred your home (or share of a jointly owned home) to a spouse or ex-spouse as part of a divorce settlement, you are considered to have no gain or loss. You have nothing to report from the transfer and this entire publication doesn’t apply to you.

Report as ordinary income on Form 1040, 1040-SR, or 1040-NR any amounts received from selling personal property. Start with the amount of real estate tax you actually paid in the year of sale. Subtract the buyer's share of real estate tax as shown in box 6.

No comments:

Post a Comment