Table Of Content

You can use Schedule LEP (Form 1040), Request for Change in Language Preference, to state a preference to receive notices, letters, or other written communications from the IRS in an alternative language. You may not immediately receive written communications in the requested language. The IRS’s commitment to LEP taxpayers is part of a multi-year timeline that began providing translations in 2023. You will continue to receive communications, including notices and letters, in English until they are translated to your preferred language. This tool lets your tax professional submit an authorization request to access your individual taxpayer IRS online account. Go to IRS.gov/Account to securely access information about your federal tax account.

Published in

Payments of U.S. tax must be remitted to the IRS in U.S. dollars. Go to IRS.gov/Payments for information on how to make a payment using any of the following options. Go to IRS.gov/SocialMedia to see the various social media tools the IRS uses to share the latest information on tax changes, scam alerts, initiatives, products, and services. Don’t post your social security number (SSN) or other confidential information on social media sites.

Publication 523 - Additional Material

If you didn’t meet the Eligibility Test, then your home isn’t eligible for the maximum exclusion, but you should continue to Does Your Home Qualify for a Partial Exclusion of Gain. You can include the sale of vacant land adjacent to the land on which your home sits as part of a sale of your home if ALL of the following are true. Also, you may be able to increase your exclusion amount from $250,000 to $500,000.

Which property do you make your primary residence?

Ms Rayner, the Labour deputy leader, has insisted that, while they were together, she lived at a house she owned on Vicarage Road. Mark Rayner, her former husband, sold his property, on Lowndes Lane, Stockport, in 2016 after purchasing the home using the right to buy scheme in 1991. The question of where she was living is crucial to determining whether she owed any tax, and if she committed electoral fraud. The Taxpayer Bill of Rights describes 10 basic rights that all taxpayers have when dealing with the IRS. Go to TaxpayerAdvocate.IRS.gov to help you understand what these rights mean to you and how they apply.

If you know of one of these broad issues, report it to TAS at IRS.gov/SAMS. The safest and easiest way to receive a tax refund is to e-file and choose direct deposit, which securely and electronically transfers your refund directly into your financial account. Direct deposit also avoids the possibility that your check could be lost, stolen, destroyed, or returned undeliverable to the IRS. Eight in 10 taxpayers use direct deposit to receive their refunds.

Rental Property

You didn’t live in the house again before selling it on August 1, 2023. Therefore, the suspension period would extend back from August 1, 2023, to August 2, 2013, and the 5-year test period would extend back to August 2, 2008. During that period, you owned the house all 5 years and lived in it as your main home from August 2, 2008, until August 28, 2010, a period of more than 24 months. You meet the ownership and use tests because you owned and lived in the home for at least 2 years during this test period.

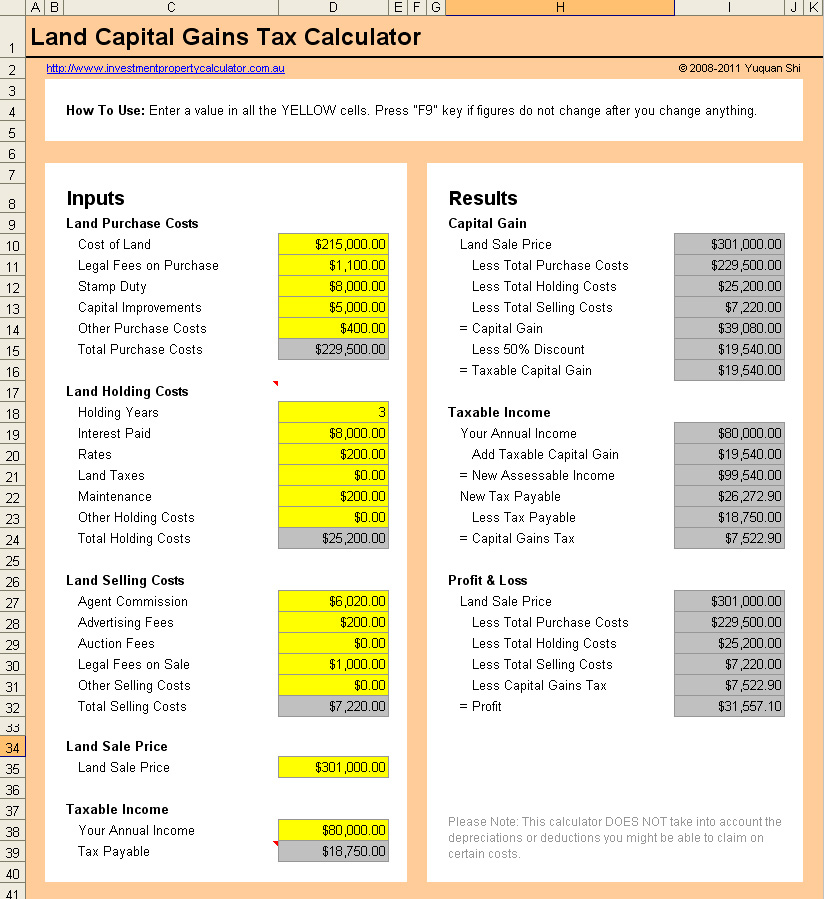

Avoiding capital gains tax on investment properties

Any differences created in the translation are not binding on the FTB and have no legal effect for compliance or enforcement purposes. If you have any questions related to the information contained in the translation, refer to the English version. Stepped-up basis is somewhat controversial and might not be around forever.

What about a partial home exclusion?

If you meet the IRS qualifications for not paying capital gains tax on the sale, inform your real estate professional by Feb. 15 following the year of the transaction. The capital gains tax is the tax individuals pay when selling an asset or capital property. That isn’t quite as cataclysmic a policy shift as referring to a blanket 44.6% long-term capital gains rate would suggest. If you used all of your home for business or rental after May 6, 1997, you may need to pay back (“recapture”) some or all of the depreciation you were entitled to take on your property. “Recapturing” depreciation means you must include it as ordinary income on your tax return. What percentage is the capital gains tax for most people selling long-term investments?

Short-term capital gains tax rates

When you have completed each worksheet, you will know whether you have a gain or loss on each part of your property. It is possible to have a gain on both parts, a loss on both parts, or a gain on one part and a loss on the other. For more information about using any part of your home for business or as a rental property, see Pub. For the next 6 years, you didn’t live in it because you were on qualified official extended duty with the Army.

Her work has been featured in Yahoo Finance, Bankrate.com, SmartAsset, Black Enterprise, New Orleans Agenda, and more. The Ascent is a Motley Fool service that rates and reviews essential products for your everyday money matters. You don't have to live in the home for two consecutive years, but a minimum of two years out of the last five. In other words, if you buy a home and sell it a year later, you can't use the exclusion, regardless of whether it was your primary home during your ownership.

So if your cost basis on your home that you own jointly with your spouse is $400,000 and you eventually sell it for $900,000, the IRS can't touch a penny of your gains. It's only when you exceed $500,000 in net profit that the proceeds will be taxed. This means that if you sell your home for a gain of less than $250,000 (or $500,000 if married, filing jointly), you will not be obligated to pay capital gains tax on that amount. Short-term capital gains are taxed as ordinary income, with rates as high as 37% for high-income earners. Long-term capital gains tax rates are 0%, 15%, 20%, or 28% for small business stock and collectibles, with rates applied according to income and tax filing status. Your basis in your home is what you paid for it, plus closing costs and non-decorative investments you made in the property, like a new roof.

Liz Weston: Tricky capital gains exclusions can cause confusion, vary due to state of residence - OregonLive

Liz Weston: Tricky capital gains exclusions can cause confusion, vary due to state of residence.

Posted: Sun, 21 Jan 2024 08:00:00 GMT [source]

It uses the money that you lose on an investment to offset the capital gains that you earned on the sale of profitable investments. This means that you can write off those losses when you sell the depreciated asset, which cancels out some or all of your capital gains on appreciated assets. You might find that an investment property you rent out and plan to sell has spiked in value.

However, if a property is solely used as an investment property, it does not qualify for the capital gains exclusion. Capital gains tax is due on $50,000 ($300,000 profit - $250,000 IRS exclusion). If your income falls in the $44,626–$492,300 range, for 2023, your tax rate is 15%.

Continue reading to find out how your capital gains may be taxed (or not) in different situations, including a couple of ways to defer a potential capital gains tax hit. Perhaps you want to sell your main home, vacation home, or residential rental property that you own. Or you might, unfortunately, be experiencing financial trouble and are considering negotiating a short sale of your home with the bank. Other people may have had their homes destroyed in a wildfire, hurricane, or other natural disaster. You certainly don’t want to be hit with a larger-than-necessary tax bill.

Keep in mind that gains from the sale of one asset can be offset by losses on other asset sales up to $3,000 or your total net loss, and such losses may be eligible for carryover in subsequent tax years. The FMV is determined on the date of the death of the grantor or on the alternate valuation date if the executor files an estate tax return and elects that method. "I think that even middle-class Canadians could be dramatically impacted by this," said Leah Zlatkin, mortgage broker and LowestRates.ca expert, in a video interview with CTVNews.ca. LITCs represent individuals whose income is below a certain level and who need to resolve tax problems with the IRS. LITCs can represent taxpayers in audits, appeals, and tax collection disputes before the IRS and in court.

No comments:

Post a Comment